|

After two very strong months of data covering October and November,

we got one last month of strong closed sales data in December, but a

slowdown in pending sales growth suggests we shouldn’t expect a boom in

closings to start out the New Year.

Click below for the four key metrics our Windermere Economist, Jeff Tuker, watches to track supply and demand in

the market: closed and pending sales, which tell us a lot about demand;

and listings – new and active – which tell us a lot about supply.

|

|

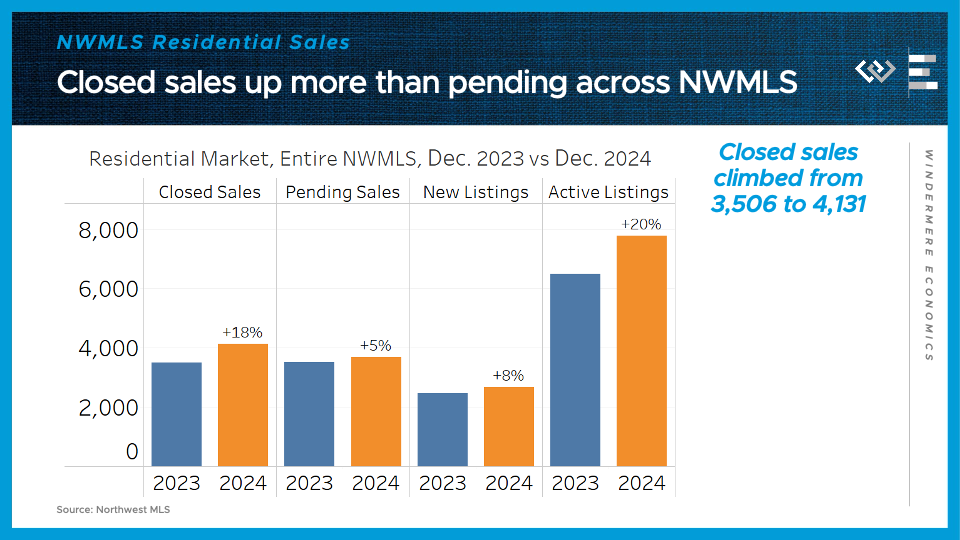

Closed sales of single-family homes climbed 18% year-over-year, from

about 3500 to over 4100. Pending sales, which will mostly close in

January, only climbed 5% from the same month last year.

On the supply side, about 8% more new listings hit the market this

December compared to last one, while the level of inventory in the

reservoir was 20% higher at the end of 2024 than at the end of 2023. Of

course this is a quiet time of the year in the market, so we should

expect all these measures of listings to pick up soon.

The final key metric to check in on: the median price for those

closed single-family home sales climbed about 5% year-over year, from

$610,000 to $639,000. That’s a bit of a cooldown from price growth in

the previous couple of months, and it’s pretty similar to the pace I’m

projecting for 2024.

|